Crowdpartners risk policy

Crowdpartners acts as a broker to set up financing. We assess finance proposals on the basis of relevant data and we verify them against general principles about responsible lending. On that basis, we determine a risk classification. A creditworthiness check or the Graydon payment assessment may form a part of the assessment. Our experienced team is able to facilitate crowdfunding projects and we have a state-of-the-art platform, the necessary licences and a solid back-office. However, it is up to you to form an opinion and to decide whether or not to accept a finance proposal.

What does Crowdpartners do?

- We critically assess every loan application, in accordance with fixed procedures.

- We determine a risk classification, we state the Graydon Payment Assessment and we check the creditworthiness score.

- Our partners manage the application and add their specific expertise.

- A Projectinformation memorandum is published for each project.

- We use professional credit documentation.

What can you do to reduce the risk to the greatest possible extent?

- Invest a safe part of your total assets in credits via crowdfunding.

- Distribute your investment in crowdfunding across multiple loans, thereby spreading your risks.

- Ensure the investment mix is good (savings, crowdfunding, shares, property, bonds, etc.).

- We advise against using borrowed money to invest.

Risk and Return

All lending involves risks and in principle, the interest rate has to be higher as the risk is greater. The reverse is also true: a high interest rate often is a sign of a greater risk. Crowdpartners will ensure that the interest rate is in a reasonable proportion to the risk classification.

Spreading your investments

We recommend only investing a safe part of your assets in crowdfunding and to spread your investments across various projects so as to reduce the risk. For non professional private investors (consumers), the maximum total investment via Crowdpartners is €80,000 in accordance with the regulations of the Netherlands Authority for the Financial Markets [Autoriteit Financiële Markten (AFM)]. This restriction does not apply to investments made by a business.

Investment profile

We recommend preparing an investment profile for yourself, i.e. to determine in advance what kinds of credits you wish to invest in and to what maximum extent. You can do this on the basis of our risk classifications and also according to sector and region. As for the risk classification, please bear in mind that the majority of applications come from smaller businesses that tend to be B2 rather than A1. An example for SME credits:

No guarantee for your investment

Crowdpartners tries to give you the best possible idea of the borrower and his prospects. The risk classifications are determined very meticulously. However, your investment remains fully at your own expense and risk and cannot be guaranteed by us, regardless of the risk classification and Graydon Payment Assessment.

Risk classification

Crowdpartners’ risk classifications are based on the information available to us at the time of the application. They are then determined in accordance with an independent methodology, trying to look one year ahead. The classification is the result of weighted scores of various factors. The most important criterion of the risk classification is that the borrower generates enough cash flow in order to pay the interest and make repayments. For business credits, we look at environmental factors (such as the prospects for the sector), business and financial risks (sustainability of profitability, the capacity to generate cash and leverage/asset structure) and management & transparency. In the case of lending to private individuals for rented property, we look at the capacity to generate a positive cash flow from rent and at the asset structure.

Probability of Default

Preparing a risk classification is a common approach in the financial world. The probability of default is assessed, that is, the likelihood of a borrower defaulting, i.e. failing to fulfil his obligations. This assessment can be expressed in an estimated bandwidth of the probability of default percentage (PD%), an assumption based on the experiences of various parties, and is linked to the score./p>

Securities

Any securities such as a first mortgage or private guarantee from an entrepreneur will be mentioned in the finance proposal. The value of a security is also determined by the status or circumstances. Examples include the location, maintenance and the use of a building, while the value of a building that is already rented out will differ from that of a building that still needs refurbishing and will be rented out in the future.

Mortgage security

On behalf of the investors, Crowdpartners will instruct a civil-law notary to create a mortgage right on the commercial property or the registered property which the loan applies to. In the event of unforeseen repayment problems with the borrower, Crowdpartners can act on behalf of the investors and in extreme cases, it can exercise the mortgage right.

Pledging

Depending on the situation, we will ask the borrower to pledge rent and buildings cover via the mortgage for immovable property or to pledge operating assets and equipment. Death cover is also an option, as this offers more security for the investors.

Subordination

If the borrower already has a credit facility with the bank and most assets have been transferred for security thereof, the lending will, in effect, be more of a subordinated nature. That means that you are not likely to get your money back in the case of liquidation, etc. unless sufficient specific securities were furnished that ‘give you priority’ such as a revolving mortgage. For every proposal, Crowdpartners will find out if, in their opinion, it concerns an actual subordination and if so, they will mention it.

Payment assessment

The Graydon Payment Assessment (www.graydon.nl) is based on information that is available at the time of the application and is adopted from the Graydon report of the borrower in question. During the term of the funding arrangement, the Graydon payment assessment is not amended if a borrower’s financial situation improves or worsens. The scores for the payment assessment are determined on a scale from 1.0 to 10.0 (the lower, the poorer) on the basis of weighted empirical facts, with negative experiences weighing heavier. The entry score is 5.5.

Creditworthiness check

Crowdpartners checks (all private) borrowers with the BKR (www.bkr.nl).

Crowdpartners:

- determines the risk classifications.

- aims for responsible financing and applies transparent rules in that respect;

- recommends only investing a safe part of your assets in crowdfunding, spreading your investments across various projects and preparing an investment profile for yourself; and

- is exempted by the Authority for the Financial Markets for acting as intermediaries with regard to repayable money pursuant to Section 4.3, subsection 4 of the Financial Supervision Act [Wet financieel Toezicht]. It also has a licence to act as intermediaries and to offer mortgage finance. Crowdpartners is supervised by and is listed in the register of the Authority for the Financial Markets (afm.nl).

Monitoring

Being an investor, you will understand that lending money to SMEs or property investors usually is a sign of a good return but you also know that risks can never be fully excluded. Also, entrepreneurs need to realise that a loan agreement means they have to pay interest and make repayments for the term of the loan.

During the term

- As soon as the loan incepts, the provisions of the loan agreement apply.

- Crowdpartners has a coordinating role in the management of a loan.

- We check the prompt receipt of interest and repayments and we will send the borrower a reminder if necessary.

- Crowdpartners notifies investors about (unforeseen) project developments in time.

- When a borrower’s financial situation improves or worsens, the risk classification or the Graydon payment assessment is not amended during the term of the loan.

- We aim to publish periodic updates (at least once a year) about the borrower’s situation in the online credit dossier you can access. If the borrower fails to provide the required periodic (numerical) data, we will send him a reminder.

- If Crowdpartners has reason to assume that the continuity of regular payment of interest and repayments is jeopardised, it will talk to the borrower. Crowdpartners will assess the nature and gravity of the situation and possible solutions.

- Crowdpartners may also suggest a possible solution to the investors. The decision is made on the basis of an ordinary majority (half + 1). The extent of participation in the loan determines everyone’s right to vote. The result of the vote is binding for all investors. Crowdpartners will then implement the decision. If costs are involved in this solution, they will, in principle, be payable by the borrower. Crowdpartners will include the costs in its proposal, especially if it involves costs to be incurred by investors.

Default

If the borrower fails to pay interest and make repayments, measures can be taken in order to collect the outstanding debt. In such cases, Crowdpartners acts in the interest of the creditors so as to secure payment for the creditors, if possible, within the possibilities and the statutory regulations. The costs thereof are payable by the borrower, to the extent they can be recovered.

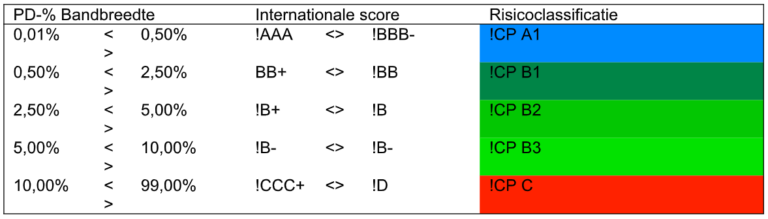

Risk classification – SME Loans

For business loans, Crowdpartners uses scores that are derived from an international classification that makes it possible to give investors a better idea of the risks involved. We express this assessment in an estimated bandwidth of the probability of default percentage (PD%), an assumption based on the experiences of various parties, and we link that to a letter & number combination:

What does this mean?

It works as follows. As the PD% rises and, as such, the risk classification, there is a bigger risk that the business is in default and will no longer be able to pay interest and make repayments. So financing with a risk classification of !CP B2 can still be wise but the risk of losing your money is definitely bigger compared to !CP A1, for instance.

Note: our risk classifications are as objective as possible. We try to give you a realistic idea of the risks. The majority of applications comes from smaller businesses that are relatively vulnerable, having to depend on only a small number of persons and having less buffer capital. That is why most of the risk classification will fall under B2.

Crowdpartners only publishes finance proposals with a risk classification of !CP B3 or better. In the case of a new business, we will clearly indicate it concerns a starter. The term and the value of security also have to be taken into account. A first mortgage (with the right of summary execution) is better than a second or a third mortgage (which does not have that right).

Crowdlease

In the case of crowdlease, we supplement our analysis with an assessment of the property in question. We include the fixed criteria which, on the basis of the description and functioning of the property to be leased, say something about the anticipated useful life, the scope of a second-hand market and the quality of manufacturer and dealers, for instance.

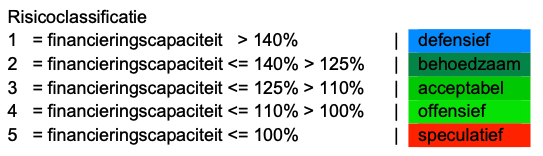

Risk classification– Rented Out Property Private Individuals

In the case of property rented out by a private individual, we use the approach below against the background of that individual’s financial situation in order to find out about the probability of default. We use five risk classifications which, ultimately, indicate the probability of a borrower defaulting.

Overview of the risk classifications of Crowdpartners:

Finance capacity refers to rental income minus (i) the average annual interest payments measured over the first five years and (ii) repayments on the basis of a 30-year term and (iii) standard 15% costs (for maintenance, for example), all in relation to the total original principal sum (i.e. without taking repayments into account) and the development thereof throughout the term. As more remains after interest and repayments, there will be more scope to absorb setbacks.

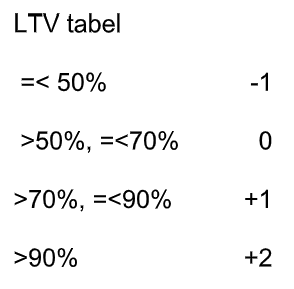

Apart from the finance capacity, we also look at the collateral value of the property because in the event of payment problems and a forced sale of the collateral, the proceeds of that sale are likely to be lower than the estimated market value. This collateral value is set at 80% of the estimated market value of the property when rented out.

This is a conservative figure. A higher collateral value will improve the risk classification only if the finance capacity is 110% or better because sufficient finance capacity is the decisive factor. A low collateral value will always have a negative impact on the risk classification. The above risk classifications (1 to 5) are applied on a step-by-step basis. We assume the Loan to Value (LTV), the ratio between financing and collateral value, and points are added to the risk classification in accordance with the table below:

Examples of adjustment risk classification:

1 with LTV < 50% is 1 (1-1, but better than 1 is not possible)

1 with LTV 60% is 1 (1+0)

2 with LTV 80% is 3 (2+1), which is shown in our project information with “3 acceptable” this:

Crowdpartners only publishes finance proposals with a final risk classification of 4 or better.

What does this mean?

As the risk classification increases, so does the risk that the borrower will default. So financing with a risk classification of 4 still be acceptable but the risk of losing your money is bigger compared to 2, for instance. The project information states important considerations that were included when determining the risk classification.

The term and the security also have to be taken into account. A first mortgage (with the right of summary execution) is better than a second or a third mortgage (which does not have that right).